Since our last quarterly installment, significant and unresolved world events have, at least temporarlily, stolen the wind from the market’s sails by introducing new variables, not the least of which is their impact on inflation, and as a result, we are seeing elevated volatility, and equally as relevant in this connected world, a spike in internet searches featuring the search term “volatility.”

Volatility measures the serverity of price changes in assets, typically by measures of standard deviations from the average price change – think of it as bookends on either side of the average. By definition, this means that volatility is measuring a moment in time relative to historical averages. Said otherwise, to determine how volatile something is today, you must look backwards for comparison.

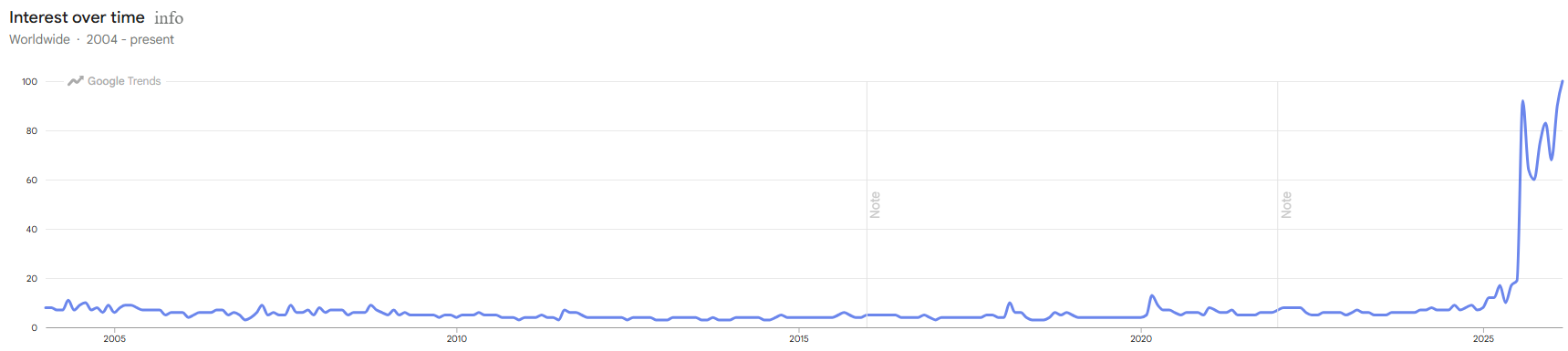

Google launched “Google Trends” in 2006, although data collection for underlying queries began in 2004. The chart below shows the relative interest in searches related to the term “market volatility”. Hits at or around 50 indicate average search interest, while hits at or around 0 indicate substiantially less than average interest, and hits at or around 100 indicate peak interest. We are currently at 100.

While the relative level is obviously extreme, the chart is not flawless. I have to imagine that factors such as expanded global internet access, a larger investing community, and social media, just to name a few, likely influence the increase in search interest for this topic. Perhaps there were different methods of information gathering in 2008? Or maybe the reality of 2008 was so obvious that nobody needed to confirm their thinking through the internet? Or maybe there is just more noise today and you feel compelled to scour the internet for answers? Whatever the case is, what does volatility actually mean for you?

What Now?

You have three options during highly volatile markets. You can sell assets, you can buy assets, or you can do nothing. First, you need to define what kind of investor you are.

Long-Term Investors: If the assets in disucssion are long-term in nature, think 5+ years, your best option is to sit still and do nothing. If you have cash that you can afford to put to work for a few years that is not comitted to any short-term obligations, market downturns can be great opportnities to buy high-quality assets on sale.

Short-Term Investors: If the assets in discussion are short-term in nature, think less than 24 months before they need to be liquidated, you probably are not in a position to be taking stock market risks. Short-term Treasurys and money market funds are your wisest option.

Speculators & Traders: I would be naïve to think that there are not at least a few people reading this that are getting ready to put on a short-term trade with high conviction. Please let this serve as a reminder to only risk assets that you can afford to lose. You can be absolutely right about a stock, but if the assets in disucssion are needed for liquidation before your thesis plays out, you could be forced to liquidate at exacly the wrong time.

In actuality, most of us are in multiple categories. Retirees should have adequate cash reserves that allow them to not sell assets at exactly the wrong time. Yet, they need to maintain an adequate level of long-term upside to compete with inflation, healthcare costs, etc. Our younger clients have all the time in the world to tolerate market volatility in their retirement accounts, but the dollars needed to fund their home rennovation, equity partnership buy-in, or new car purchase cannot have a wide range of outcomes. Each dollar needs context, thoughtful financial planning provides that context.

Tax-Loss Harvesting

When does selling make sense? Selling assets at a loss can make sense in taxable accounts. If you bought the S&P 500 ETF (IVV) a few months ago and sold it today you would generate a capital loss. Why would you take a loss on something you intend to hold for decades? Selling IVV at a loss and simulatenously reinvesting the proceeds into a competing S&P 500 ETF (VOO) keeps you fully invested in an identical exposure, all while generating losses that can be used to offset current and/or future capital gains.

For “frozen” portfolios with highly appreciated ETFs, or highly appreciated concentrated stock positions, ask us about long/short direct indexing. Long/short direct indexing can provide substantial pre-tax and post-tax alpha that traditional long only direct indexing and ETF portfolios cannot attain. Investors should be aware that long/short indexing comes with more complexity than traditional long-only investing. Risks including leverage levels, portfolio margin, financing costs, short-selling, and tracking error which in some cases can be substantial.

In summary, market pullbacks present opportunities as well as distractions. Our advice is to revisit your financial plan with myself, Austin or John for context and lean on your us to help you determine what course(s) of action are most sensible for your situation.

Having a plan not only allows you to ignore a lot of the noise we are seeing right now but it also gives you personal context and peace of mind in times of increased market volatility.

Summit and its affiliates do not provide tax or legal advice. Please consult with your tax and/or legal advisors before taking any action that may have tax and/or legal implications.